NurPhoto/NurPhoto via Getty Images

Jefferies highlighted the relatively unknown beneficiaries of a booming weight loss drug market last week after Novo Nordisk’s (NVO) parent agreed to acquire the U.S. contract manufacturer Catalent (CTLT) with an eye on supporting the Danish drugmaker’s obesity drug business.

When the $11.6B Catalent buyout closes later this year, Novo (NVO), the maker of diabetes and weight loss drugs Ozempic and Wegovy, is expected to acquire three CTLT fill-finish sites from its parent, Novo Holdings.

Thermo Fisher (TMO) and its Swiss rival Lonza (OTCPK:LZAGF) (OTCPK:LZAGY), along with Catalent (CTLT), operate in the fill and finish segment of the weight loss drug market, where Novo (NVO) and its U.S. competitor Eli Lilly (NYSE:LLY) dominate with their GLP-1 drugs.

Pfizer (PFE) and Amgen (AMGN) are among other GLP-1 drug developers aiming to grab a piece of the obesity drug market, which, according to Morgan Stanley, could reach $77B by 2030.

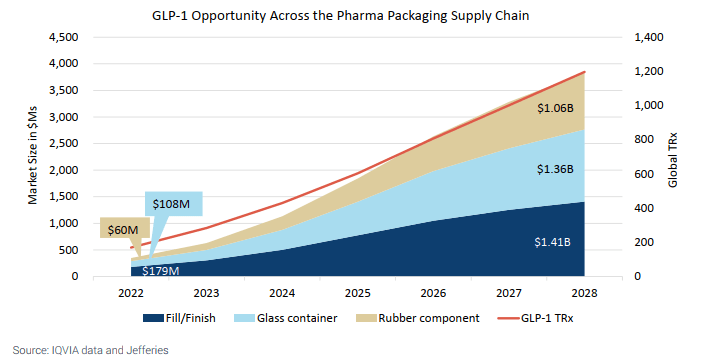

Meanwhile, Jefferies estimates that “pick-and-shovel” plays in the obesity drug market, including those focused on the fill-and-finish process of manufacturing, will represent a $3.8B opportunity by 2028, as GLP-1 scripts hit ~1.2B up from 284M in 2023.

“Recent FDA approvals of GLP-1s to treat obesity are expanding dramatically the opportunity for the manufacturing supply chain,” Jefferies analyst David Windley wrote.

According to Windley, contract manufacturers like Thermo Fisher (TMO) and Catalent (CTLT) will likely lead GLP-1’s fill-and-finish process as their smaller rivals struggle to meet the technology and capacity required by the industry.

He added that rivalry is high in the injectable fill/finish market, where low margins and fierce competition are among key characteristics, and the number of players is in the 10s rather than in the single digits.

Societal CDMO (SCTL), Rovi (OTCPK:LABFF), and Pfizer (PFE) are among other notable operators in the fill-and-finish manufacturing process.

Additionally, with newer GLP-1 requiring disposable, pre-filled pens for delivery, Windley highlighted opportunities for key glass and rubber vendors in the GLP-1 market.

The analyst added that the growing number of FDA-approved injectables is another tailwind for the industry.

Rising demand for cartridges and pre-filled syringes used to deliver GLP-1s is leading to over double-digit growth for many pharmaceutical-grade glass suppliers, such as Becton, Dickinson (BDX), Stevanato Group (NYSE:STVN), and Gerresheimer (OTCPK:GRRMF) (OTCPK:GRRMY), according to Jefferies.

The GLP-1 glass market is expected to reach ~$1.4B by 2028, up from $197M currently, the firm argued, raising its price target on Stevanato (STVN) to $32 from $29 per share. However, the analyst remained Hold-rated on the Italian firm due to softness in demand for some of its products unrelated to GLP-1s.

Jefferies estimates that the market for rubber components linked to GLP-1 drug delivery could grow from $130M in 2023 to ~$1.1B by 2028, mainly benefiting West Pharmaceutical (NYSE:WST), which claims to have over 90% exposure to the segment.

Dätwyler (OTCPK:DATWY) and AptarGroup (ATR) are other operators. Still, WST dominates both, Windley added as he upgraded the Exton, Pennsylvania-based firm to Buy from Hold, raising its price target by as much as 66% to $536 per share.

The upgrade comes as West (WST) is scheduled to release its Q4 2023 results this week, with analysts expecting it to report ~$3.0B for last year with ~5% YoY growth. However, according to the consensus, the company’s 2026 revenue is expected to rise ~11% YoY.

“GLP-1s will require a global footprint with plenty of capacity. WST has that, and we think neither Aptar nor Datwyler are likely to take meaningful share of GLP-1s at their smaller scale,” Windley wrote.